Doing The FINRA Jig

A Documented Journey

Don't Let This Happen To You

| The following is an account of actual events. The stock advisor, broker, places and names have been omitted. |

Positioning:

It was the summer of 2013. My wife and I had a REIT that became liquid. Our REITs were investments made around six years ago from rolling over 401ks and pensions when we had worked, the full amount of this one REIT in two checks from an IRA.

Over those six years, as a retired couple, we were able to receive a monthly distribution of 7% to 8% to add to our cost of living beyond Social Security for a nice gain of about 42% on our original investment. Again, that original investment was now being returned to us in checks we would send to a new broker situated in a mid-Atlantic state for reinvestment into another IRA.

The original broker of the REIT was located in the northeast where we had lived and worked for well over two decades. Having been with this broker for over 12 years investing in other REITs, we decided to invest with a different broker in the geographic area where we recently retired. We wanted to compare the brokers to see if the new one would provide better services with an equal or better monthly distribution to continue supplementing our cost of living.

As former school teachers who entered the business world late in our lives while having raised six children, we still have a mortgage and now live in a small retirement home. Our basic living budget is as follows:

23.7% (mortgage / utilities / home repairs), 7.1% (communications / digital services), 6.1% (auto insurance / repairs / gasoline), 8.2% (medical, annual advantage coverage), 8.2% (groceries), 12.4% (driving vacations, gifts to family, entertainment + eating out, misc Jesus factors), 4.8% (donations), 9.5% (federal and state taxes), and 20% (savings to pay off our mortgage.)

We own two used cars and have zero credit card debt with no other outstanding loans. Our credit rating is 800. Our mortgage is 3.6% fixed 30-year loan that our bank, by coincidence, bought up from another lender. We have no other assets outside our home, cars, and REITs investments that are not in the stock market other than the one in this discussion.

So with our budget we're still able to make cuts if necessary. While our REITs are called high risk, we had watched mutual fund investors lose 20 to 30% of their investments in safe stocks in the 2008 crash while we didn't lose a dime.

However, as other REITs become liquid probably this year, we plan to begin investing in other areas that will include around a 7% distribution. That should provide us with enough money outside our social security to pay for a rest home in the next decade if it would become necessary. We don't want to turn over our assets to the government for sub-standard retirement living after seeing our parents go through that with the little money they had and institutions keeping them semi-drugged 24/7.

Our Instruction And Goal To The New Broker:

Our two IRA checks had been mailed to the new broker so that our hands would never touch the money, allowing us to show on our 2014 taxes the investment had gone into another IRA.

The broker was part of a large banking firm that already had our savings, checking, and our mortgage along with a trust division to execute our will. We thought with that much business, the bank's stock broker would look after us with a keen eye.

We had our first meeting, after the checks had been deposited with the broker, to discuss our goals. One goal, which we didn't discuss with him, was for a one-year investment to see the results of his actions and decisions to protect our retirement money. With other REITs becoming liquid possibly at the end of 2014, we needed the information as to which broker was the best to watch over our retirement money.

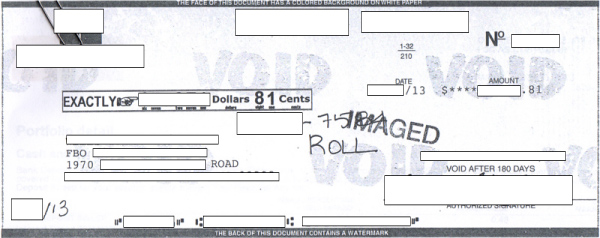

Copies of the two checks sent to the broker from the REIT that became liquid

Again, the REITs we were in had NOT been related to the stock market, an investment we understood that needed to mature while we worked. After around six to seven years with an excellent monthly return on distribution, each REIT would be made available for sale to a third party. As a point of information, in the case of a former REIT it was bought by the huge real estate investor.

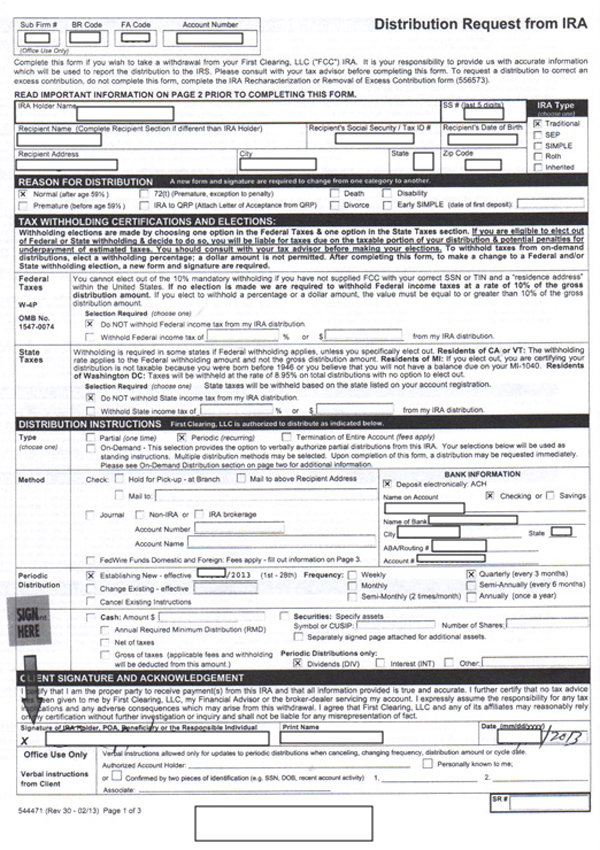

Once this current REIT was sold, the investment was made liquid and returned to us as cash for reinvestment. Since it was an IRA, the cash was moved (see form below) and reinvested as an IRA with the new broker.

We advised the new broker we were interested in another REIT with at least an equal distribution we could depend on for our living costs and savings to pay off our mortgage. We told him we hadn't been near the stock market for 12 years and wanted to know if there was a way to protect our IRA investment.

He told us there was a way. He called it a stop loss.

He told us a stop is set if the stock were to drop down to a certain level, protecting the investment we were entrusting him with. He never said where that stop would be or who chose it, our therefore thinking it might be a computer action.

He told us he preferred safe bonds or mutual funds that might get us a distribution of 4% or less. But we said as long as the stock he would recommend was not expected to go belly up, (we know there are no guarantees), we had no problem with a REIT.

Our investment had already grown with our 401ks and pensions. We were looking instead for distribution in retirement, understanding that what goes down can come back up. But with a stop loss we figured a loss would be minimal allowing us to get out and look into another investment.

He first recommended one REIT, then a few days later changed his mind to another with a 11% distribution every three months. We accepted his trust to watch over our hard-earned IRA that we were putting in his hands. He then invested our money in a company called DX Capital around June 10th, 2013, the value at 10.1

We went on our way thinking not much more about the transaction, looking forward to our first distribution at the beginning of November. That is the way it was with our original REITS for over 12 years, again those not in the stock market.

History Of Investment And Later Discoveries:

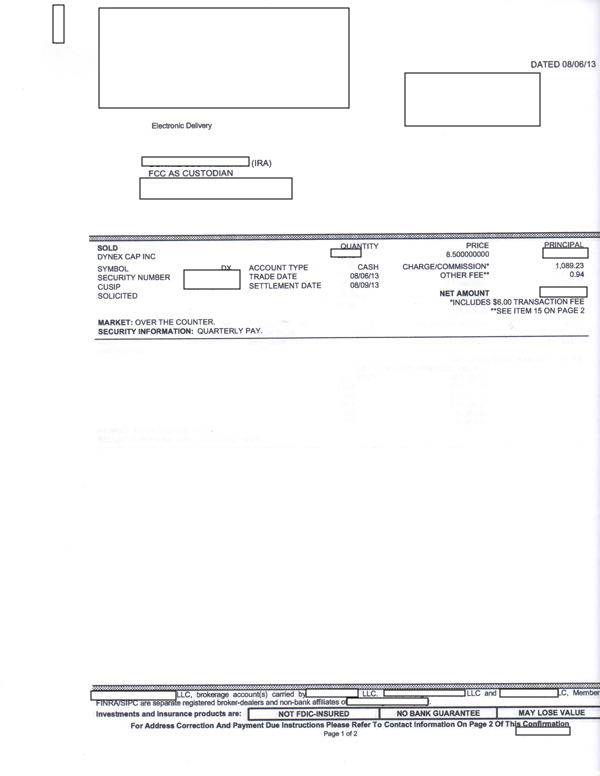

Then on August 6th, (according to exact records we didn't have until February of 2014), our stock hit its first stop loss. The broker called us and asked for permission to sell and hold. I said fine per his advice in protecting our investment.

I asked him what the stop loss was that triggered this event. He said it had reached 9. We had bought the stock at 10.1, so that was at least a ten percent loss in our investment. I asked him why it was set so low to allow that much loss of the investment we had given him. I said I thought a stop loss was to protect the investment by not allowing it to drop that much.

Then on August 23rd when the stock rose again, he bought it back setting a new stop loss. Meanwhile we hadn't seen any e-mails on the transactions and didn't think any more about it, believing all had finally settled down.

Then nearly two months later on November 5th, (again according to exact records we didn't have until February of 2014), he sold the stock again when it reached the next stop loss. This time the stock was below 8.5. In a few days he bought the stock back when it went up.

Then about three weeks later when watching the stock online, I saw it drop to 7.9. This time I called the broker and asked, "Did you drop in a stop loss?"

He said the stock had gone back up to 8.0.

I said, "But what if it had gone down instead to 7.5?"

Then I asked something with new concern. "How much are these stop losses costing us? I've seen online trades on television well under $100 dollars a trade."

The broker laughed on the phone and informed me these trades cost thousands of dollars.

I was stunned, not knowing what to say on the phone. He must have picked up on my silence and realized he had never told us the price of these stop losses or maybe didn't want to. I write this because we would find out later after filing a complaint that the stop loss actually had another name. It was called a 'broker's commission.'

He broke the brief silence on the phone and said, "I have a pit in my stomach. I'll tell you what. On the next stop loss, I'll eat it."

I replied, "Eat what? We never knew these stop losses were costing us thousands of dollars. And the stop loss was to protect our investment. We bought at 10.1 and now the stock is at 8.0. How did your suggestion back in June protect our money?"

I then said, "No more stop losses." The stock later dropped to 7.3, and then started to rise again past 8.0.

Because of my discovery of what a stop loss was, I began to wonder if the broker had recommended a stock he knew would hit the stop losses to create commissions for him since the cost was never mentioned.

In early December with a pit in my stomach, I called my bank's national phone number, asking how could I find out who would be responsible for managing a broker. They gave me the e-mail of a regional manager. After I e-mailed the question to the regional manager, he then e-mailed the area manager, who then had his assistant contact me. The assistant later said he could file a complaint with the compliance district for the area, asking what our complaint was. I indicated that while the stock had gone down that wasn't my complaint.

My complaint was that the broker had told us a stop loss would protect our investment. Not only did it not protect our investment, now losing well over 20% of our funds, but he was charging us thousands of dollars we were not aware of. This cost was not discussed in the original meeting in June, nor at the stop losses. You would think he would have said on the phone at the first stop loss, "You know this is costing you and your wife thousands of dollars." But those words never came out of his mouth for any stop loss.

It was getting near Christmas and the assistant manager had finally contacted the compliance division of the bank. At the same time I began to investigate, trying to educate myself in other stocks that would have met our original request with the broker in June.

I first looked at the DX stock for five years, a chart provided online. Here is where we bought it back in June. Look at the hand on the chart.

Then I looked at the same stock on its five-year chart. Below is what I found. I was stunned. Not only looking at the stock's five-year history, one could easily see the stock was probably ready to go down.

But then I looked at the stock the broker selected with its full history shown. What I saw was unbelievable. (see below.)

I discovered in this graph the stock started in 1990, rose to over 50 points and then dropped in February of 2001 (see upper left of chart) to a value less than 1, or 69 cents. The stock started to rise slowly again reaching 10 points in February of 2008. Six years later our broker would recommend it for our investment with it showing little to no growth for six years. Stunning stuff.

Our broker never showed us these easy-to-read charts on the past history of the stock. He instead, at a meeting near our home, gave us a mound of paper we had no idea how to read.

Moving on to January 2014, two letters arrived from the regional compliance office concerning our complaint to the assistant manager, the first one written January 13, 2014. It was encouraging. We were looking for a resolution for the cost of the stop losses we had not been advised of by our broker in June or during the stop losses themselves.

The next letter arrived, written January 29, 2014. I was surprised, as no one from the bank's compliance office ever contacted us for details on our original complaint. Here is what it read:

Our bank had stunned us again. The letter read that the broker's fees "had been fair and competitive," and therefore our complaint had no justification. However, the broker's fee being fair and competitive was never the issue. The issue was the broker had never, from June through November, advised us what those fees would be.

I then e-mailed the area manager's assistant and asked that we be removed from our broker so no more funds could be taken from our account, now almost a third of our investment gone. We still didn't know the extent of exactly what those stop loss fees were or how many were activated. I thought two, maybe three. I also asked for a few recommendations of other brokers who could take over our account in the investment location closer to our home.

On February 18, 2014, my wife and I met with the area manager, who said he was now taking over our account and wanted us to sell what was left of our investment and put it into a safe fund with maybe 4% distribution. While the manager tried to look like a hero by taking over the account, we would later discover that it is basic bank procedure for the area manager to take over a troubled account.

In the meeting with the assistant manager in attendance, I told the manager that I had looked at other similar REITS and was shocked at what his broker had sold to us last June. I found four other stocks that had done better than the DX he recommended with two actually making money based on comparisons.

He pushed my comment off, saying it didn't matter, that the investment we had for 12 years was a risk and we should never have invested in it. I told him the distributions came every month without fail and without losing a dime when the market crashed in 2008 and many mutual funds lost close to or over 1/3 of their value. I explained that the reliable distribution covered our cost of living since we had retired to the area.

He assured us that he was protecting us and suggested we cut our living expenses to get by with 4% or less distribution. Since we had been living off of 7% and 8% since we retired over 7 years ago, that would mean cutting our costs by 50%. We still have a mortgage that we want to pay off with the distributions, which would give us $650 more dollars a month.

We left the meeting feeling slapped around at 73 years old. Again, there was no response as to why the broker had never told us the stop losses were several thousand dollars each or why the broker didn't give us other options to invest back in June of 2013.

While preparing the following information for the meeting, I accidentally noticed when online viewing the DX stock there was a button labeled, More stocks like this.

Wow. I couldn't help thinking our broker could have done this with little effort. In June he had never given us a choice of other stocks and never showed us these online trends you are about to see.

Below is what I found online. I showed the estimated balance of these four other stocks at the area manager's meeting matched along with the DX stock the broker had recommended to us, the investment time from June 10 to February 14th on all five for apples to apples.

When looking at the online stock charts below, note if the NMM had been recommended back in June we would have probably not had any stop loss with the value of our investment increased at the same time. The same for the stock, MCC. The other two would have lost us money but $3,000 less than the stock the broker had recommended. All provided quarterly distributions of 9 to 13 percent.

Finally, when at the meeting the manager still didn't know how much we lost in stop loss fees to his broker, thinking possibly $5,000 for six incidents. But the next day I contacted his assistant manager using e-mails. He had always been helpful and exhibited the behavior that I would have expected from the bank toward a loyal customer. I needed to know the answer that no one had given to me. Exactly where were those commission costs that were supposed to have come to us? I could never find them in my e-mail.

He said that the broker might have assumed, (a very bad word in the corporate world), that since we were online we knew how to find the costs of the broker's commissions.

After the assistant manager and I e-mailed each other a few times, I finally got the instructions on how to find the cost of the commissions. Without being trained by the broker back in June, there was no way I would have found the cost of his commissions because of all the screens necessary to get to those final charges. The process is nothing at all like the ease of online banking.

So how easy was it to find the stop loss commissions vs. online banking?

The online banking screen lists all your accounts at the bank. Simply clicking, for instance, on your main checking account takes you immediately to your checks and deposits. But the investment activity screen was a whole different ball game. We were shocked no one had taken us through it until near the end of our adventure.

First, when you get to the investment screen you see the value of your investment, but there is no link to see commissions. On top of the Web page are 17 tabs. One of those has the commissions. In my earlier clicking on each of them in attempts to find the commission charges, I found two tabs were errors that took me offline.

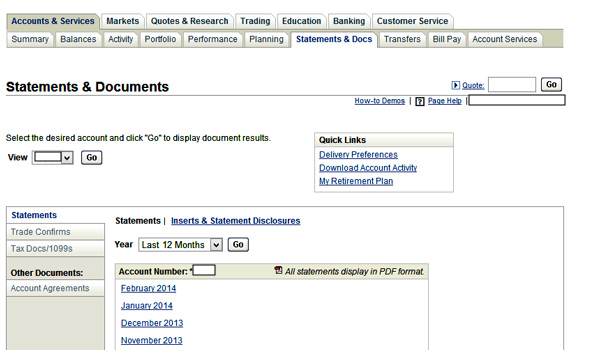

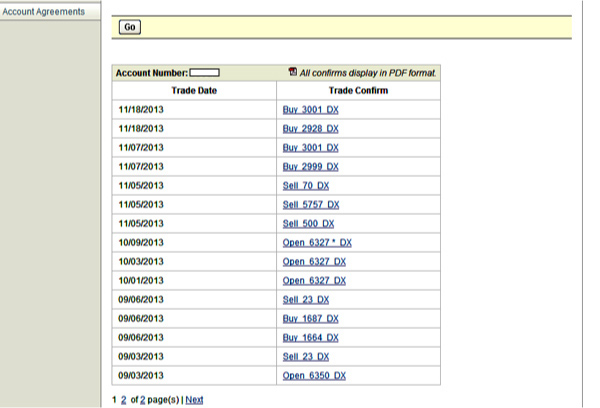

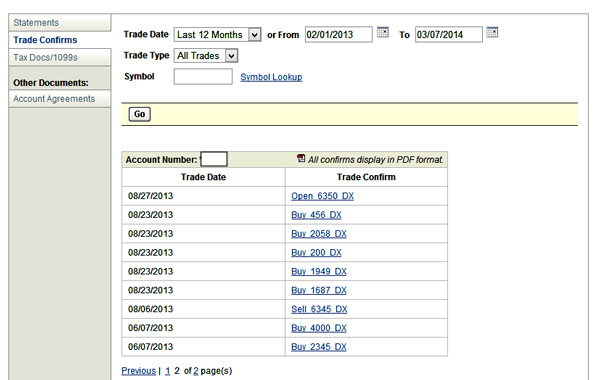

I discovered with the help of the assistant manager that the tab I was supposed to click on was "Statements and Doc." Then under that tab I thought I would look for commissions or stop losses. Those words were not there. The correct link on the page, I discovered with the assistant manager's help, required scrolling down and looking for the link labeled, "Trades." Once clicking on that word, I saw activities by date for "buy, sell, or open."

There were 24 incidents on two pages by one account. As a novice we would have had to know the exact dates of the stop losses to pick the correct ones out of the 24 while ignoring "open," coming up with either four instances for two stop losses or six for three.

So after eight months I would finally discover the cost of those trades and how many were made. First, here is how the online banking looks. Click on any blue link and your account comes up. That's it.

Now for the broker screen. Watch how this screen is nothing like the online banking. There is no way anyone would assume if you knew online banking you could just breeze through it and find the cost of the broker's commissions. Check this out.

First you have to go to the broker tab that brings up this screen.

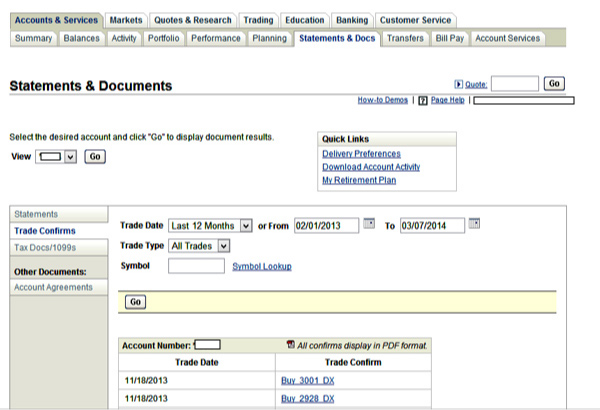

Then under the above screen you have to find and click on "Statements and Docs."

Then you don't look for the word commissions or stop losses, instead the words, "Trade Confirms." Click on the link.

Then to find all the trades by date, you scroll down on the same page to see the following.

But note the message on the bottom of the screen, page 1 of 2, so you have to click on 2 to complete the list of activities since June 2013.

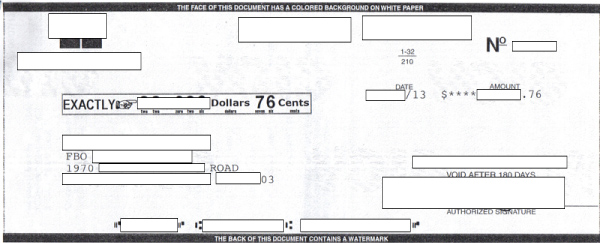

From these two screens you have to then determine how many trades and how many buys from the 24 activities listed, obviously ignoring "open." I had no idea how to read these, some canceled, some for around $100. The assistant manager looked at all 24 at his office, as I was looking on screen at home. He wrote back saying there were four incidents, two sells and two buys for each account. He told me the dates to look for. I then went to those four, printing the following report for one "sold" activity on August 6th.

There were three more forms, one matching this one with a "BUY" and then four more on the other investment account for the same SOLD and BUY dates. That gave me a total of four incidents, not six, for each, as had been speculated in the meeting. And the cost against our account for broker commission and fees was not $5,000, but over $6,100 and change.

Several weeks later at the end of February, I got a call from the legal department at the bank, telling us that the compliance department was no longer involved. I was happy to hear that because they never got it right in the first place."

The manager for the legal department then asked me what I wanted.

I said, "While we understand we have to live with the stock he advised us to buy, even though he never gave us several choices with stats laid out, we would like to have our $6,000 returned based on false information or actually the lack of it over an eight month period . . . that even the area office manager didn't know the final amount until about two weeks ago."

The manager on the phone said she doubted that would happen. I replied with the basic facts saying in effect . . .

"Whatever you decide, investors need to know how easy it is to lose thousands of dollars through information hidden by a broker while his employer protects him at all cost. Therefore, I think I should inform the investing public on the Web what my wife and I went through, and that if a broker says stop loss and doesn't give a cost, run out the door."

I also told her FINRA, (Financial Industry Regulatory Authority), might also be interested in how a large bank was operating in FINRA's field of regulations, not advising customers the meaning and cost of a stop loss. But that may be for another day in the near future. The manager seemed irritated, but I always like to lay my cards out so that no one can say later they didn't know.

In the end looking over what had happened, the broker had put the first stop loss without ever advising us at 9, after we had bought the stock originally at 10.1. As I have shown in this report, for the NMM stock a stop loss would probably never have been needed while we would have increased our investment. We thought the stop loss would have been put under but close to the value of the stock, so we could take a breath to see where it was going with only a minor loss. But the area manager in the meeting said in defense of the broker he would have put the stop loss at 9. So there you go with respect for client information out the window.

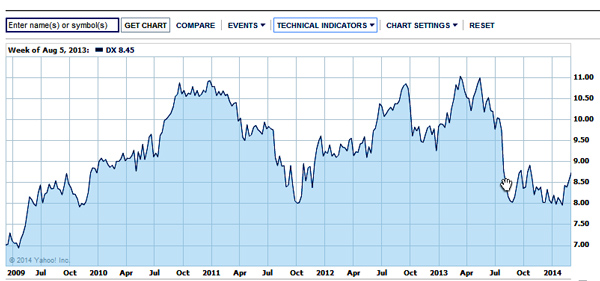

However, what I didn't discuss with anyone is the chart below for the first stop loss. As you saw in the above commission report, it was dated August 6th, supposing to have sold our stock when it dropped to 9. But look at the DX chart for August 5th, the day before and its value shown in the upper left part of the screen is $8.45.

On August 5th the stock was already below 8.5, forget 9. In fact it had already dropped below 9 before July 29th. See the hand below in the chart, the upper left showing the value of the hand at $8.78 on July 29th.

In summary, our investment is now down to around 70% of value. The $8,000 annual distribution we were looking forward to receiving was going to pay for our federal and state taxes in April of 2014. But because of the stop loss charges, actually commissions by our broker, that $8,000 was trimmed to $2,000, with $6,000 going to line the pockets of the broker and the bank.

We had already received $4,000 of the distribution, now eaten up by the stop losses. The final $2,000 is expected at the beginning of August of 2014. Today is March 7, 2014.

As Paul Harvey would say, And that's the rest of the story.

Finalized edits 3/7/2014, 11 P.M.

Background Graphic Sources: | Bilbos Random Thoughts (BoGrace) | Trading Game (Wizard of Id) | Carrier Management (Bird) |